- English

- 中文版

- Launch webtrader

Launch webtrader

- Ways to trade

Ways to trade

- Platforms

Platforms

- Markets & Symbols

Markets & Symbols

- Analysis

Analysis

- Learn to Trade

Learn to Trade

- Pepperstone Pro

Pepperstone Pro

- Partners

Partners

- About us

About us

- Help and support

Help and support

Analysis

Week Ahead Playbook: Sentiment Solid As Jobs Day Approaches

The Week That Was – Themes

The policy ‘put’ was in full effect for the second week running last week, with Chinese authorities picking up the stimulus baton after the FOMC’s ‘jumbo’ 50bp cut to kick-off the easing cycle a week prior.

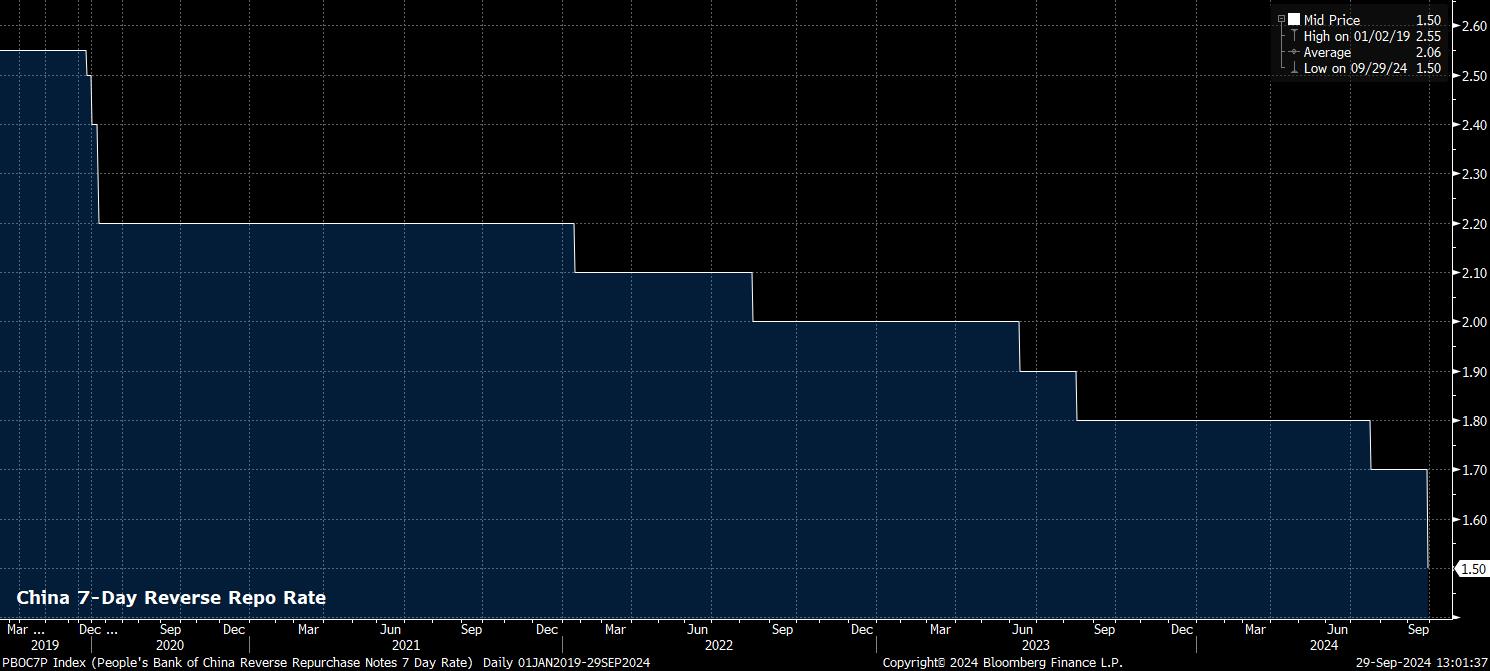

It appears that the Chinese Government’s pain threshold, both in terms of material economic weakness, and equity market drawdown, had been breached, with a veritable bazooka of stimulus measures being unveiled as last week progressed. These included:

- A 20bp cut to the 7-day reverse repo rate, to 1.50%, coupled with a pledge to implement further “forceful” rate cuts, and a cut to outstanding mortgage rates

- Establishment of a liquidity facility allowing banks and brokers to tap PBoC fund to purchase equities, as well as discussion over a potential ‘stock stabilisation fund’

- Injection of $142bln worth of capital into major domestic banks

- A pledge from the Politburo to ensure “necessary” fiscal spending is implemented

Naturally, markets reacted positively to this slew of liquidity and stimulus, as the CSI 300 notched a near-16% gain, its best week since 2008, while the Hang Seng vaulted over 10% higher.

Nevertheless, I remain sceptical of the China bull case, for a couple of reasons. Firstly, the aforementioned issues are very much targeted towards stabilising/boosting financial markets, as opposed to resolving real-world economic issues; it is tough to argue that any of the above will allow China to exit its debt-deflation spiral, and almost impossible to argue that any of them will resolve long-running demographic issues in the world’s second largest economy.

Secondly, is the ‘elephant in the room’, that to invest in China, is to invest in a market where, even if minimal, there is a chance that one day the Government will decide that they no longer wish to respect your property or ownership rights, as has ben seen several times in the past. My long-running view of not touching the Chinese market with a 10ft bargepole remains in place.

That said, it was not only in China where stimulus was delivered, or hinted at, last week.

The Riksbank, as expected, delivered another 25bp cut, taking rates to 3.25%, with said move accompanied by relatively dovish guidance nodding towards a cut at each of the remaining 2 policy meetings this year, with policymakers also flagging that larger 50bp moves remain “possible”.

Concurrently, the Swiss National Bank (SNB) also announced a 25bp cut last week, taking the policy rate to 1.00%, as the SNB approach the effective lower bound at a worryingly rapid rate. Despite this, Chair Jordan, and incoming Chair Schlegel, noted that further cuts “may be necessary” in coming quarters, with said cuts in fact highly likely, particularly in order to avert any significant strengthening in the CHF, though policymakers remain willing to be “active” as necessary within the FX market.

It was, though, in Europe where things were perhaps most interesting last week as, although ECB policymakers very much stuck to the now-familiar ‘data-dependent’ script, incoming economic data continued to sour.

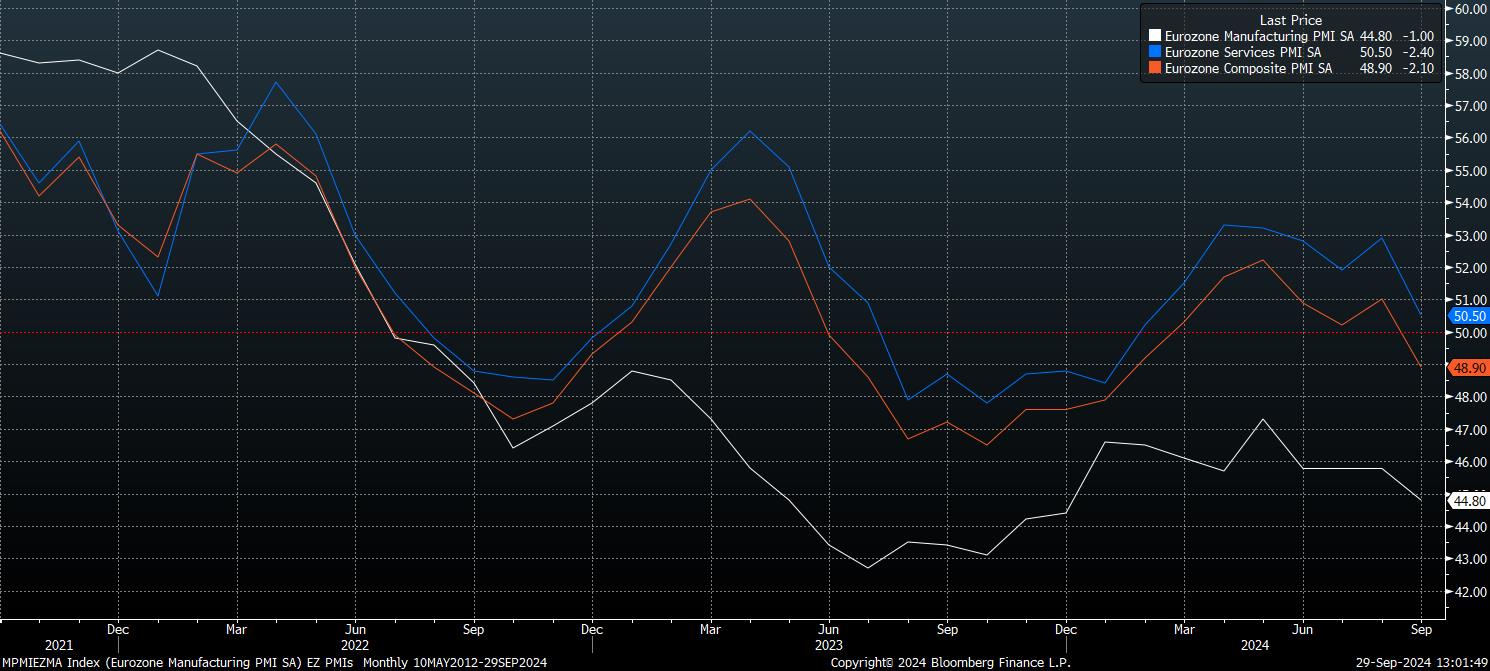

The latest round of ‘flash’ PMI surveys were rather disastrous, with manufacturing output contracting at its fastest rate in 9 months, and the services sector expanding (barley) at its slowest pace in seven months. Overall, the composite output gauge slipped below 50.0, into contractionary territory, and to its lowest level in 8 months.

Perhaps unsurprisingly, given the willingness of policymakers elsewhere to act quickly amid signs of deteriorating economic momentum, money markets have undergone a significant dovish repricing, now seeing around a 80% chance of a 25bp ECB cut next month, compared to around a one-in-three chance this time last week. This week’s inflation report will be key to cementing the likelihood of back-to-back cuts, though cooler-than-expected figures last week from France, and Spain, imply the balance of risks tilting towards cool bloc-wide figures as well.

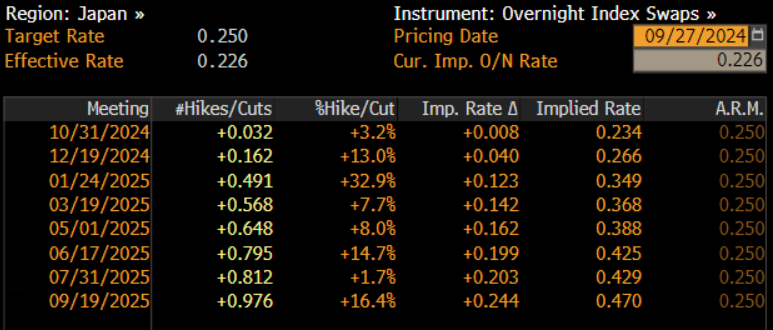

Back in Asia, Japan’s LDP leadership election, eventually, produced the most market-friendly result, with former defence minister Ishiba emerging victorious at the fifth time of asking, in a run-off against Takaichi, a notable voice against further BoJ tightening. Ishiba’s victory seems unlikely to materially alter the BoJ outlook, with a further hike likely this year, probably in December.

Stateside, the week lacked major economic releases, at least market-moving ones.

The latest initial jobless claims report showed claims hovering around a 4-month low, at 218k, though continuing claims, in the week coinciding with the September NFP survey week, rose a modest 5k to 1.834mln. Meanwhile, the August core PCE report painted something of a mixed picture – while the index rose just 0.1% MoM, modestly slower than consensus expectations, the annual rise of 2.7% YoY was a touch quicker than the 2.6% increase seen in July.

All that said, the PCE data matters relatively little, with the FOMC having already obtained sufficient confidence in inflation returning towards target on a sustainable basis, over the medium-term, hence leaving labour market figures as the primary determinant of policy moving forwards.

The Week That Was – Markets

The strengthening of the global policy ‘put’ seen last week acted as a fillip for risk appetite last week, with equities across the globe once more rallying strongly, and a series of major benchmarks notching fresh record highs.

The S&P 500 rallied for a third straight week, with notable outperformance coming through in the tech sector, as the Nasdaq 100 also notched a third weekly advance, clambering north of the 20,000 mark once more. A fresh record for the Nasdaq is well within sight, as the path of least resistance continues to lead to the upside, and dips continue to be viewed as buying opportunities.

The three supporting pillars of my long-running bull case remain intact – strong economic growth, solid earnings growth, and the forceful Fed ‘put’ continuing to underpin risk sentiment, providing participants with confidence to remain further out the risk curve.

Record highs were not restricted to Wall Street, though with the DAX surging over 4% on the week, notching its own fresh all-time high north of the 19,000 mark. This rally is a classic example of how ‘the stock market is not the economy’ – incoming German economic data has been about as dire as one can imagine, with last week’s IFO business climate index slumping to its lowest level since January, yet the market has continued to gain ground, on expectations of an increasingly loose ECB stance.

In keeping with the general trend seen since the GFC, at their heart, equities remain a pure liquidity proxy.

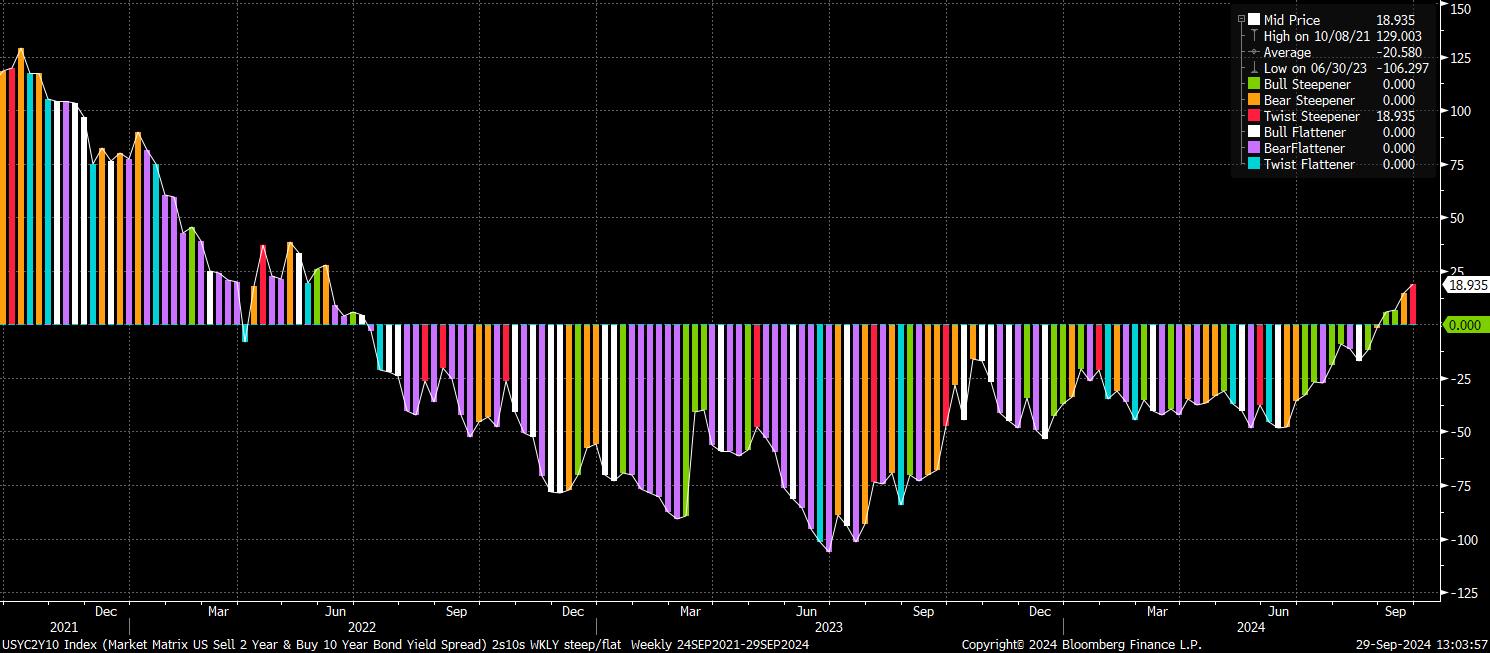

Away from the equity space, the Treasury curve continued to bear steepen last week, with front-end yields slipping to fresh YTD lows amid a modest further dovish repricing of Fed policy expectations, while the long-end continued to sell-off. The 2s10s, consequently, steepened north of 20bp, to its widest since mid-2022.

With the market having absorbed supply well last week – as 2- and 5-year auctions stopped on the screws, and the 7-year auction stopping through by 0.7bp – continued selling at the long-end remains an apparent reflection of participants’ concern that policymakers could well be running the risk of easing policy too much, too soon, into an economy that remains resilient.

The front-end rally once more posed relatively stiff headwinds to the greenback, with the dollar index (DXY) notching a 4th straight weekly decline, and printing fresh YTD lows at 100.15.

Interestingly, the G10 FX world has shifted from an environment where ‘buying growth’ was the preferred strategy, albeit in a low vol environment, to one where it is the pace at which rates will return to neutral that has become the market’s main focus. In this light, the greenback seems likely to face continued headwinds, with Powell & Co having positioned the FOMC at the front of the queue to remove restriction in relatively rapid fashion, particularly compared to DM peers. In contrast, the GBP, AUD, and NOK remain primed to outperform, given the relatively slow pace of easing likely to be followed by the three respective central banks.

For the buck, though, the DXY has continued to grind towards the bottom of its 2-year range around 99.60. Selling rallies towards this level remains my preferred play for now.

_2024-09-29_13-05-15.jpg)

As the buck has continued to soften, gold has remained attractive, with the yellow metal advancing just shy of 1.5% last week, notching fresh record highs in the process, and gunning towards a test of $2,700/oz to the upside. Gold, in my view, remains a momentum play, with it being tough to fade the rally just yet, even if ‘traditional’ fundamental drivers of the PM space point to the rally being on somewhat shaky ground. Silver also advanced last week, briefly touching its best levels since 2012.

Lastly, crude once more displayed a ‘buy the rumour, sell the fact’ reaction to incoming geopolitical, and weather-related news, with WTI slumping over 5% on the week, trading back below $70bbl – Saudi Arabia reportedly abandoning their $100bbl Brent target also shan’t have helped sentiment.

My view remains that sustained upside in crude requires a durable pick-up in global demand, which thus far remains elusive. Selling rallies down to the 2023 lows around $64bbl still seems a reasonable idea.

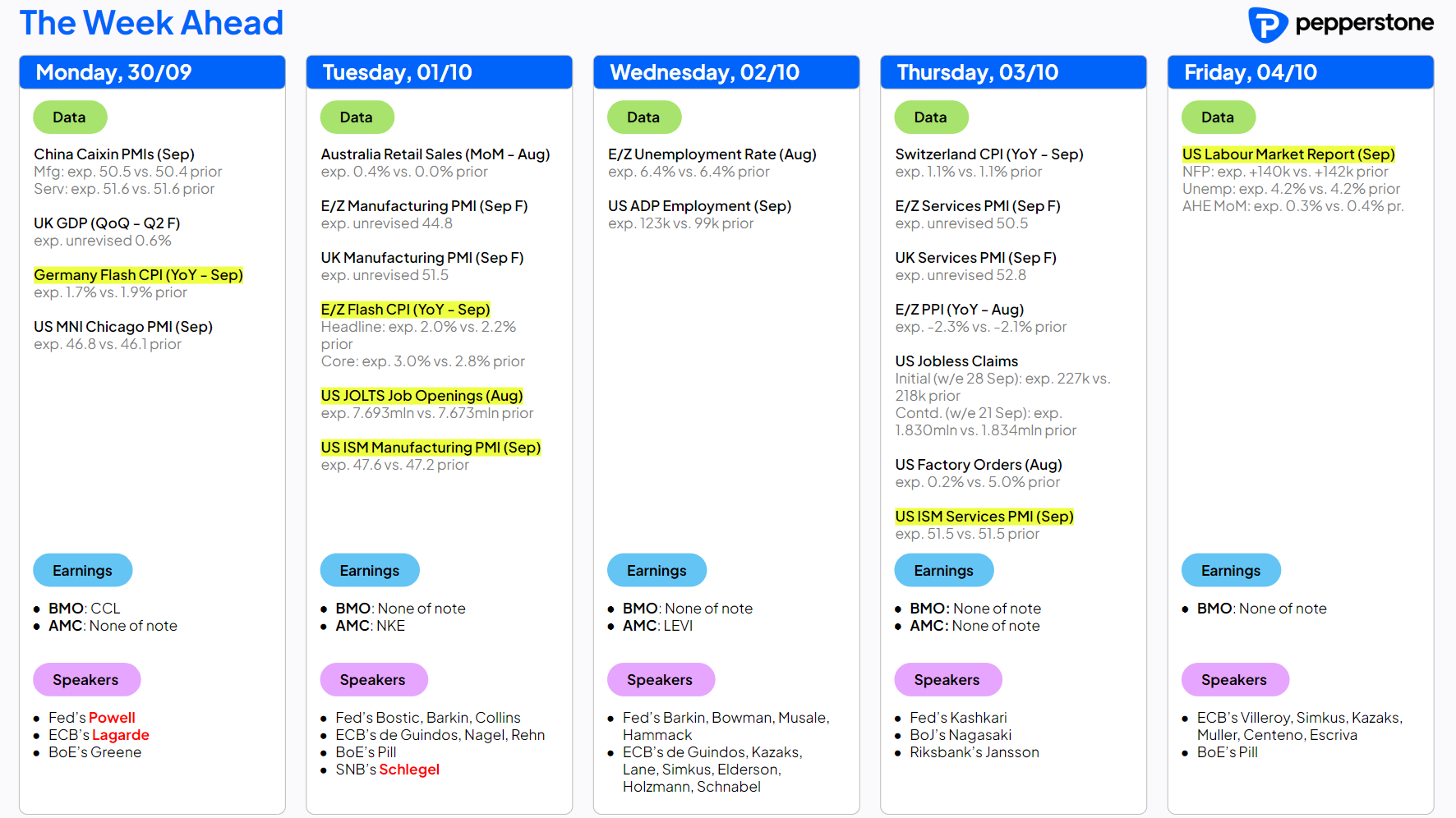

The Week Ahead

A busier data docket awaits this week, as the final quarter of the year gets underway, and the calendar presents plenty for participants to get their teeth into.

As is typically the case, the first Friday of the month brings our latest read on the state of the US labour market, with September’s jobs report this week’s main event. Headline nonfarm payrolls are seen rising +140k, broadly in line with the pace seen a month prior, and consistent with a continued gradual normalisation in labour market conditions. Unemployment, meanwhile, is seen unchanged at 4.2%, with participation also likely to hold steady, though earnings pressures are set to moderate a touch, with average hourly earnings set to have risen by 0.3% MoM.

Naturally, with the FOMC squarely focused on the employment side of the dual mandate, the jobs report is perhaps the most important event between now, and the next policy meeting in early-November. Any further labour market softness, particularly if joblessness seems set to rise north of the median SEP 2024 and 2025 expectation of 4.4%, is likely to be met with a significant dovish repricing of the USD OIS curve, and could also provide another brief equity dip for longs to buy into. Before the NFP print, August’s JOLTS job openings figure is due, along with the September ADP employment number, though the latter tends to bear little-to-no resemblance to the official NFP data.

Elsewhere, Tuesday’s eurozone inflation data will be closely watched, as a continued easing in energy and goods prices is set to see headline HICP hit the 2.0% YoY target per the ‘flash’ September reading. Such a figure is likely to solidify expectations that the ECB will indeed deliver a 25bp cut at the October meeting, with another such move likely to follow in December, even if core CPI is expected to tick 0.2pp higher to 3.0% YoY over the same period, as services prices remain relatively sticky.

Besides that, a slew of PMI surveys dominate this week’s docket, with the ISM manufacturing (Tues) and services (Thurs) gauges likely to be of most interest to participants. Monday’s Chinese PMIs may also be worth a look, given the stimulus recently delivered, though usual caveats with Chinese data must apply.

The earnings slate, in contrast, is relatively barren, lacking any major reports, with the start of Q3 earnings season still around a fortnight away. Finally, geopolitical developments will remain in focus, particularly amid continued tensions in the Middle East, which show no sign of ebbing any time soon.

Related articles

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted..